Disclaimer: This content is for informational purposes only and does not constitute financial or legal advice. Regulations regarding KiwiSaver, personal lending, and insurance are subject to change. Always consult directly with your KiwiSaver provider, lender, employer, and insurer before making financial decisions.

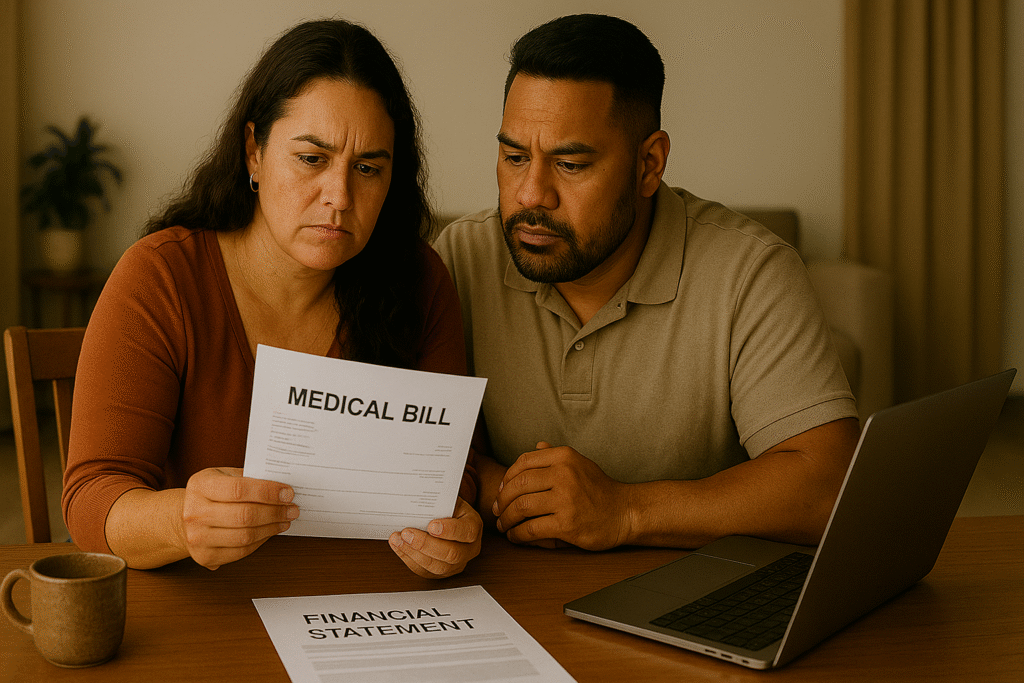

When you’re facing a long public health waiting list and considering medical treatment abroad, the first question is often: how do I pay for this?

This guide explains the realistic funding options available to New Zealand residents seeking treatment overseas. It covers what’s possible, what’s difficult, and what regulatory hurdles you’ll need to navigate. This is not financial advice—it’s information to help you understand your options and ask the right questions.

The Reality: Most People Self-Fund

Medical treatment abroad is almost always self-funded by New Zealanders. There is no government subsidy for elective overseas procedures, and accessing existing savings or taking out commercial loans are the most common pathways.

The good news is that treatment in India costs significantly less than private care in New Zealand, Australia, or the United States. A cardiac procedure that might cost $80,000–$120,000 privately in New Zealand could cost $10,000–$20,000 in Chennai, including hospital stay, surgeon fees, and post-operative care.

Even with flights, accommodation, and recovery costs, the total expense is often a fraction of what the same treatment would cost privately at home. That said, it is still a substantial amount, and planning how to fund it properly is essential.

Option 1: KiwiSaver Early Withdrawal

KiwiSaver is designed for retirement, and accessing it early is deliberately difficult. However, there are two health-related withdrawal provisions: Significant Financial Hardship (SFH) and Serious Illness. These have different eligibility criteria and allow access to different portions of your savings.

Significant Financial Hardship (SFH) Withdrawal

This is the more common pathway but also the most restrictive. SFH withdrawal is treated as a last resort by Inland Revenue and your KiwiSaver provider.

What qualifies:

You must prove you are unable to meet minimum living expenses, facing mortgage enforcement, or need to pay for necessary medical treatment. The word “necessary” is critical.

If the treatment is available through the public system in New Zealand—even with a 12–18 month wait—you must demonstrate why waiting is not reasonable. Evidence that delaying treatment would result in permanent loss of function, unbearable pain, or significant deterioration strengthens your case. A letter from your GP or specialist supporting urgency is essential.

You must exhaust all other options:

This is a regulatory requirement. Before accessing KiwiSaver under hardship rules, you must show you have explored and exhausted:

- Personal savings

- Borrowing capacity (bank loans, personal loans)

- Support from family

- Employer assistance (if applicable)

You may need to apply for a personal loan first, even if you don’t intend to take it out, to demonstrate borrowing isn’t viable. If declined, that evidence supports your application.

How much can you access:

If approved, you can only withdraw your own contributions and your employer’s contributions. You cannot access:

- Government contributions (including the $1,000 kick-start)

- Fee subsidies

- Interest earned on your account

The amount is capped at what your provider deems necessary to relieve immediate hardship—often three months of minimum living expenses and overdue bills, not the full cost of overseas treatment.

SFH is unlikely to cover your entire medical cost. It may cover part of it or help manage living expenses whilst you’re away, but it’s not designed to fund large elective procedures in full.

Serious Illness Withdrawal

This provision has a much higher threshold but significantly broader access to funds.

What qualifies:

You must provide medical evidence that you have an illness, injury, or disability that:

- Permanently affects your ability to work, or

- Is life-shortening and reduces your life expectancy below age 65

This is not about urgency or waiting lists. It’s about whether your condition has fundamentally and permanently changed your capacity to work or your expected lifespan.

Examples that might qualify: advanced heart disease where you cannot return to full-time work, terminal diagnoses, or severe degenerative conditions. Elective orthopaedic procedures, even if debilitating, are unlikely to meet this threshold unless they’ve resulted in permanent incapacity.

How much can you access:

If approved, you can withdraw some or all of your total KiwiSaver balance, including:

- Your contributions

- Employer contributions

- Government contributions

- The $1,000 kick-start (if applicable)

- Fee subsidies

- All interest earned

This makes Serious Illness withdrawal significantly more valuable than SFH—but the eligibility bar is correspondingly much higher.

Approval process:

Both applications require medical evidence and are assessed by your KiwiSaver provider under IRD regulations. Approval is not guaranteed, and the process can take several weeks. Begin early and be prepared for possible decline.

Considering treatment in Chennai? Connect with our team to discuss costs, timelines, and what support looks like from consultation through recovery.

Option 2: Personal Loans and Medical Finance

For many New Zealanders, a personal loan is the most practical and immediate way to fund overseas medical treatment. Unlike KiwiSaver, which requires proving hardship, a personal loan depends primarily on your income, credit history, and ability to repay.

Loan amounts and terms:

Typical loan amounts range from $3,000 to $50,000, though some lenders may approve up to $100,000 depending on your circumstances. Loan terms generally range from six months to five years, with some offering up to seven years for larger amounts.

Interest rates:

Interest rates on unsecured personal loans typically range from 7.99% to 24.99% per annum. The rate you’re offered depends on:

- Loan size and term length

- Your credit score

- Your income and employment stability

Advertised rates from major banks often sit around 13–14% p.a., but individuals with strong credit may secure lower rates, whilst those with limited credit may face rates at the upper end.

Repayment flexibility:

Most New Zealand lenders allow flexible repayment schedules (weekly, fortnightly, or monthly) and do not charge early repayment fees. This is important if you’re using a personal loan as bridge finance.

Example: if you take out a $15,000 loan for surgery costs and later receive a KiwiSaver withdrawal or funds from another source, you can pay the loan off early without penalty, significantly reducing total interest costs.

Managing loan repayments post-treatment:

Factor repayments into your recovery planning. Most people underestimate how long they’ll be off work or on reduced income after surgery. Ensure you can meet repayments even if your return to work is delayed or you need extended recovery time.

Option 3: Employer Support

Your employer is not legally required to pay for your medical treatment, but discretionary support may be available—particularly if the treatment allows you to return to work sooner.

Why would an employer contribute:

If you’re facing a 12–18 month public waiting list and your employer is managing your extended absence, the business cost can be significant: lost productivity, temporary staffing costs, or potential recruitment needs.

If overseas treatment can reduce your absence from 18 months to 8–12 weeks, your employer may see value in contributing as a return-to-work strategy.

This is not an entitlement—it’s a discretionary business decision. However, it’s worth discussing openly, particularly if you work in a specialised role or your absence creates operational strain.

What to provide:

- Letter from your specialist outlining your condition and prognosis

- Expected public treatment wait times in New Zealand

- Expected recovery timeline if you proceed with overseas treatment

- Evidence that treatment will enable return to full duties

Transparent communication increases the likelihood of support, whether financial or simply holding your position open whilst you travel and recover.

Limits: Your employer is not expected to make changes causing unjustifiable hardship to the business. Employer support, if offered, is goodwill—not legal obligation.

Planning Your Funding Strategy

Most New Zealanders funding treatment abroad use a combination of sources:

Assess total costs:

- Surgery and hospital fees

- Flights (patient + companion)

- Accommodation (pre- and post-surgery)

- Meals and daily expenses

- Medications and follow-up care

- Contingency fund (15–20% buffer for unexpected expenses)

Identify available resources:

- Personal savings

- KiwiSaver (if eligible)

- Borrowing capacity

- Employer support (discretionary)

- Family support

Sequence your funding:

- Use personal savings first (lowest cost, no approval needed)

- Apply for personal loan if savings insufficient

- Apply for KiwiSaver withdrawal only after exploring commercial borrowing

- Discuss employer support early, but don’t rely on it

Build in contingency:

- Assume recovery takes longer than expected

- Budget at least 15–20% more than base surgery cost

- Ensure loan repayments manageable even if off work longer than planned

Note on travel insurance: You’ll need comprehensive travel insurance for your trip—this covers unexpected emergencies unrelated to your procedure, but won’t cover the surgery itself.

A Final Word

Funding overseas medical treatment requires careful planning and realistic expectations. The regulatory frameworks around KiwiSaver, variability in loan approval and interest rates mean this requires proper preparation.

That said, thousands of New Zealanders successfully fund and undergo treatment abroad every year. The cost savings compared to private care in New Zealand are substantial, and the quality of treatment in centres like Chennai is comparable to what you would receive at home.

If you are considering treatment in India, we can help you understand realistic total costs, provide documentation to support funding applications, and connect you with patients who have navigated this process before.

The financial challenge is real, but it is manageable with proper planning.

Gaudham Pragadesh

Gaudham is the founder of Anvita Medtours, helping international patients access safe, transparent, and high-quality medical care in India. His work focuses on simplifying treatment planning, reducing costs, and providing personalised support for patients and families travelling abroad for healthcare.

“Clear information, honest pricing, and compassionate care form the foundation of every patient journey.”